Swaps are a type of derivative that allow parties to exchange the cash flows from one party's financial instrument for the cash flows of the other party's financial instrument - in a way that benefits both parties in the transaction. These two parties are called counterparties, and the streams of cash flows they exchange are called the legs of the swap. Typically a financial institution will act as an intermediary for the parties engaged in the swap, taking a spread from the payments between the two parties.

Interest Rate Swaps

Interest rate swaps allow the two counterparties to exchange interest-rate payments with each other. Typically, interest rate swaps are called vanilla swaps, and they allow one counterparty to exchange a fixed interest-rate payment for a floating interest-rate payment. The notional amount refers to the value of the loan that is subject to the swap. Unlike forwards, futures or options, a vanilla swap will not require parties to exchange the notional amount.

In fact, interest rate swaps are by far the world's most popular derivative, with a notional amount related to interest rate swaps of around $300 trillion dollars (several times the world's GDP). Interest rate swaps are used to hedge against fluctuations in interest rates. For example, a firm that has cash flows that vary with interest rates may prefer floating interest payments, and a firm with fixed cash flows may prefer fixed payments. Interest rate swaps are also used by speculators who believe the market is going to go one way of the other.

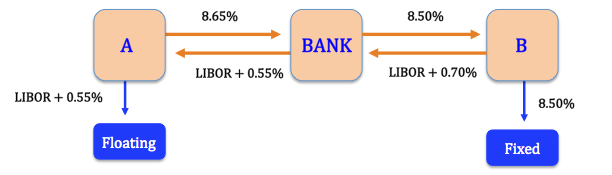

In our example, party A must pay a floating rate of LIBOR + 1.50% and party B must pay a fixed rate of 8.50%. If party B wants to pay a floating rate, it will enter into an agreement with the bank to pay the bank LIBOR + 0.70% in exchange for fixed payments on its loan of 8.50%. If party A wants to pay a fixed rate, it will pay the bank 8.65% in exchange for floating payments of LIBOR + 0.55%. The bank profits by taking a spread (the difference between LIBOR + 0.55% and LIBOR + 0.70%, as well as the difference between 8.50% and 8.65%).

Currency Swaps

Currency swaps occur when two parties swap interest rate payments and/or principle payments for the equivalent payments in another currency. This may be done for two reasons:

1. Hedging: Imagine a US company, Company A, wanted to open up a new factory in Canada. It may take out a Canadian bank loan to finance the factory. To hedge its foreign exchange risk, it may want to swap its Canadian interest-rate payments for American ones, so that its payments are always in its own domestic currency.

2. Comparative Advantage: Since Company A is based in the US, it can get a US loan much cheaper than a Canadian one. However, it needs Canadian dollars to open its new factory in Canada. This company may take out a US loan and swap its principle and/or interest rate payments with a Canadian company with a Canadian loan that needs USD. When both the principle and interest rate payment are swapped, the parties are effectively borrowing on each others behalf, and this is called a back-to-back loan. The two parties can also exchange the principle of the loan only at a fixed rate for some future date. These swaps are known as FX-swaps and are more akin to forward or future contracts.

Valuing a Swap

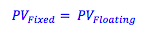

Vanilla swaps are typically priced so that the present value of the fixed legs of the swap are equal to the present value of its floating legs (less the spread that the intermediary institution takes). As a result, the swap has no value to either counterparty and no payments trade hands when the swap is entered into.

The present value of the fixed leg is the present value of the fixed coupon payments known at the time of the swap. The present value of the floating leg is calculated by discounting future interest payments using the appropriate forward rate for each payment. Analysts use what they call a multi-curve framework to estimate the appropriate forward rates to discount each future payment.

Because forward rates and discount rates may change, the present value of the different legs of the swap may change over time. When this happens, the swap becomes an asset to one party and a liability to another. Swaps are marked-to-market, and corporations that own swaps must include them on their balance sheet when their value deviates from zero.

Photo by Ethan McArthur on Unsplash

© BrainMass Inc. brainmass.com June 26, 2026, 8:04 pm ad1c9bdddf