Stock-based compensation plans have been used increasingly by companies over the last thirty years. The main benefit of stock compensation (rather than a regular salary and bonuses) is that it helps tie the employees’ interests to the long-term success of the company. Company’s also like stock-based compensation because it does not require the company to pay out any cash. On the contrary, stock options if exercised may bring in cash for the company.

The two most common types of stock-based compensation plans are:

1. Direct award of stock

2. Stock options

Direct Award of Stocks

A company may choose to directly award stock to its employees as part of a compensation plan. In the past, because this was a non-monetary transaction, companies were not required to expense stock-based pay. Today, any stock awarded to an employee as compensation must be expensed at its fair value.

Employee Stock Options

Stock options are often granted for two reasons. The first, known as employee stock option plans, are granted for the purpose of raising capital and giving employees a chance to participate in the ownership of the company. The granting of employee stock options is seen as a capital transaction and is charged to shareholders’ equity as follows.

* If the options were never exercised, any funds that were received by the company on the sale of the options would remain in Contributed Surplus.

Compensatory Stock Options

The second type of plan is known as compensatory stock option plans. These plans are seen as an alternative to compensation, and are charged to operating income for the year as a compensation expense. Compensatory stock options plans must be measured using fair value. This is true even though most options are not traded, and are difficult to value. Stock options should be valued using an option-pricing model such as the black-scholes model.

The fair value of options granted in lieu of other compensation should be expensed in the periods during which the employee renders service to the company (otherwise known as the service period). The service period typically runs from the grant date (the day on which the options were granted and should be measured) and the vesting date (the day on which the employee no longer must work for the company in order to exercise his or her options. Like most options, stock options typically also have an expiry date, after which they can no longer be exercised.

At grant date: $50,000 worth of stock options is granted to an employee for service to be rendered over the next year. If they are granted on June 30th, 2013 half of the stock options should be expensed at the end of this year (December 31st) and the other half should be expensed at the end of the employees term on June 30th, 2014.

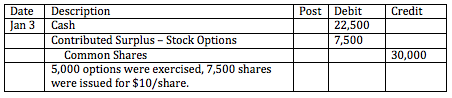

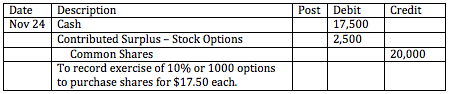

At exercise date: When the stock options are exercised, the value of common shares increases. Contributed surplus is decreased and the cash account is increased by the amount that the employee pays for the shares under the option.

At expiration: If not all the stock options are exercised by the expiry date there would be a balance in the contributed surplus account. Many companies move this balance to a separate contributed surplus account related to expired stock options.

Stock-Based Compensation

BrainMass Solutions Available for Instant Download

Fair Value of Stock Options

Do you think the fair value method is an accurate way for an organization to recognize compensation expense related to the options?