Brownian motion and Ito's formula

Not what you're looking for?

Hi, I've attached 2 questions in one file. Thanks.

Question 1 hints:

Hint 1: you have a process Y and a function, the first instinct should be to try Ito.

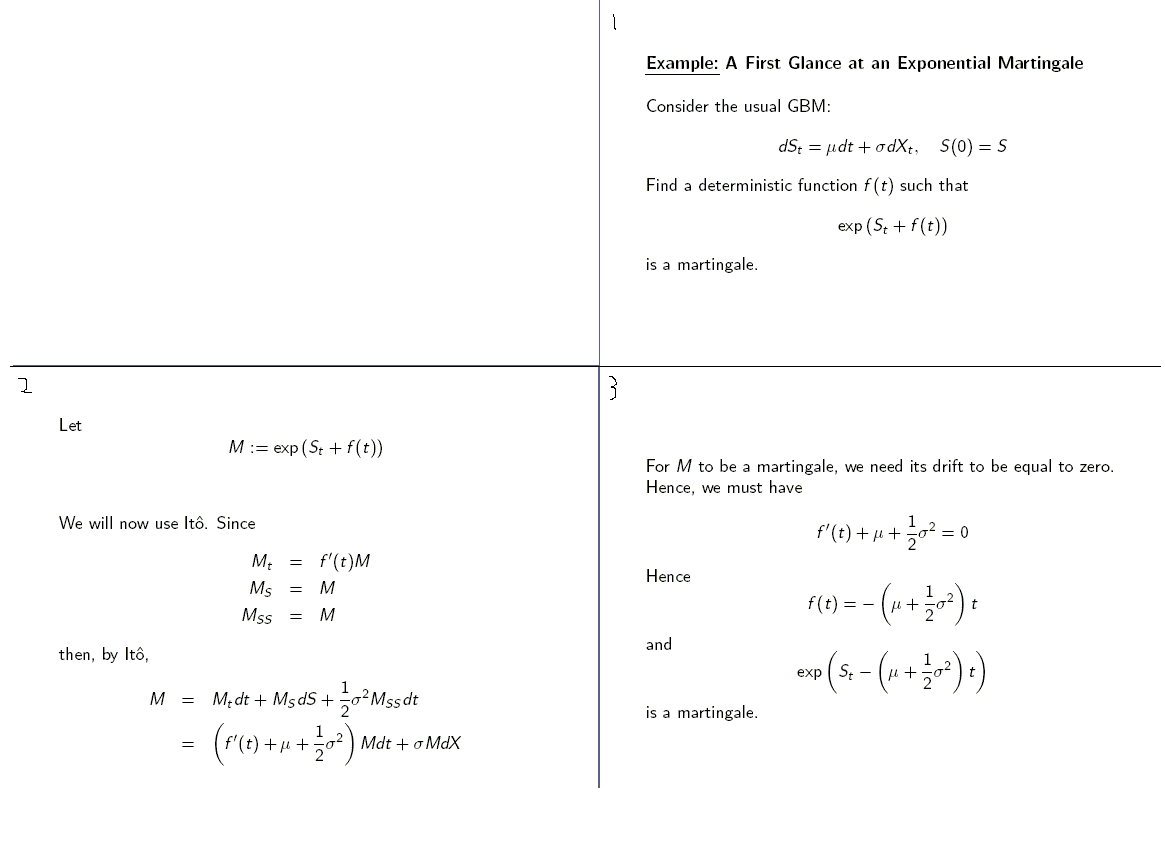

Hint 2: what would the SDE of a martingale look like? Look at attached lecture note.

Question 2 hint:

Hint: use the integral version of Ito's formula.

{kind=link}

{kind=link}

Purchase this Solution

Solution Summary

This provides an example of working with Brownian Motion and Ito's formula.

Purchase this Solution

Free BrainMass Quizzes

Exponential Expressions

In this quiz, you will have a chance to practice basic terminology of exponential expressions and how to evaluate them.

Graphs and Functions

This quiz helps you easily identify a function and test your understanding of ranges, domains , function inverses and transformations.

Probability Quiz

Some questions on probability

Solving quadratic inequalities

This quiz test you on how well you are familiar with solving quadratic inequalities.

Geometry - Real Life Application Problems

Understanding of how geometry applies to in real-world contexts