maximize utility

Not what you're looking for?

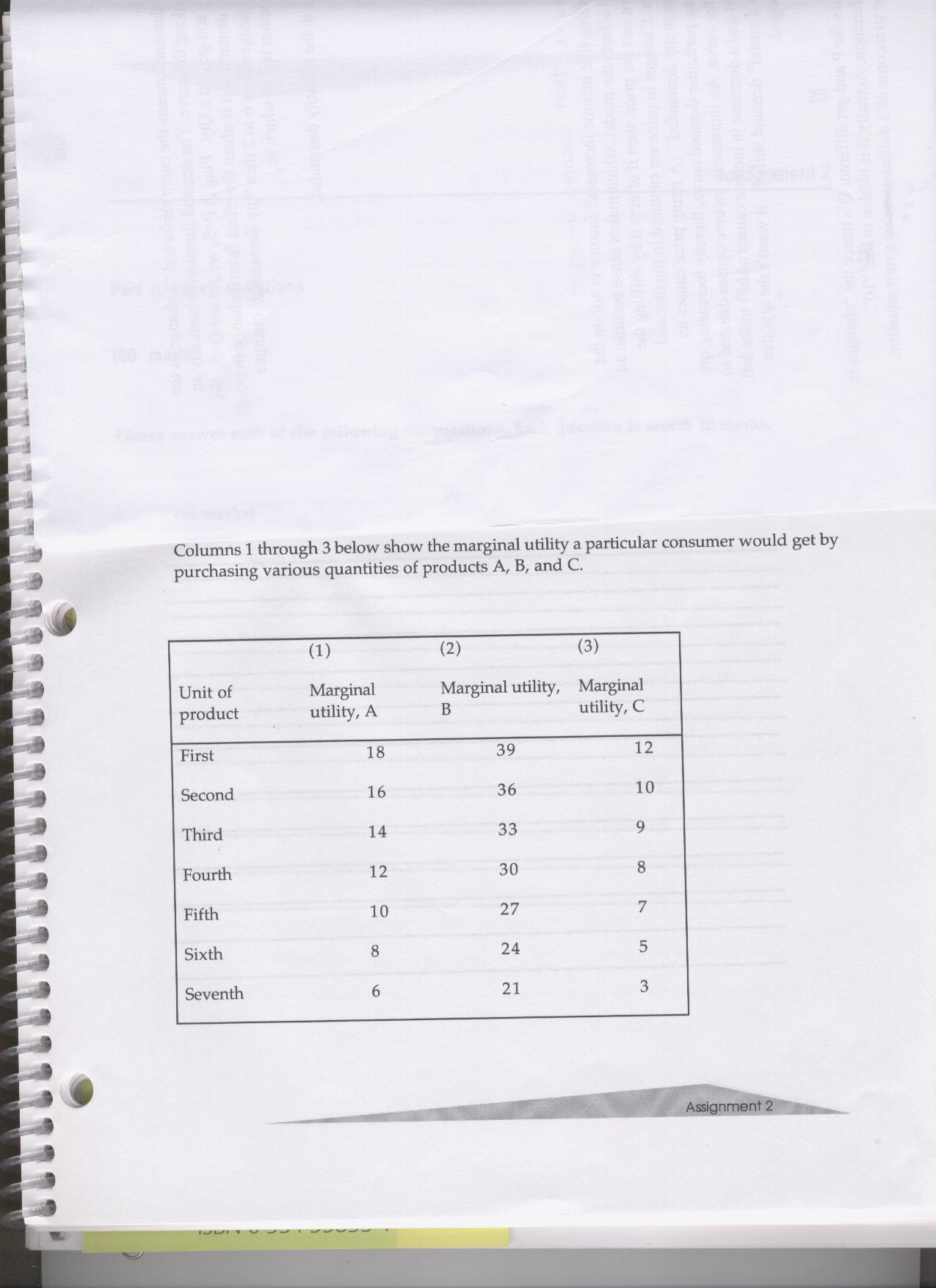

1.

If the prices of A, B and C are $2. $3, and $1 respectively, and the consumer has $26 to spend on these three products, what combination of the three products should be purchased in order to maximize utility? Please show how you get the answer.

(Please see file attached)

2.

Can you explain and illustrate with graphs( 2 of them), the relationship between the MC curve and the supply curve of a perfectly competitive industry.

3.

The long run supply curve will tend to reflect the behaviour of production costs as an industry expands when more firms enter the industry. An increasing cost industry has an upward sloping supply curve.This is based on the assumption that as new firms enter, factor prices are bid up through the competition of more firms for the limited factor services.

Could you please explain why the long run supply curve can be downward sloping and the implication for the behavious of price as demand increases over the long run. Please illustrate this with graph.

{kind=link}

Purchase this Solution

Solution Summary

This job shows how to maximize utility.

Solution Preview

answer to 1: In order to maximize utility, you need to first rank per dollar marginal utility and the pick from the highest to lowest. The result is that you buy 2 units of A, 6 units of B and 4 units of C. This will give you total utility 262, the highest utility possible with $26. ...

Purchase this Solution

Free BrainMass Quizzes

Basics of Economics

Quiz will help you to review some basics of microeconomics and macroeconomics which are often not understood.

Economic Issues and Concepts

This quiz provides a review of the basic microeconomic concepts. Students can test their understanding of major economic issues.

Elementary Microeconomics

This quiz reviews the basic concept of supply and demand analysis.

Economics, Basic Concepts, Demand-Supply-Equilibrium

The quiz tests the basic concepts of demand, supply, and equilibrium in a free market.

Pricing Strategies

Discussion about various pricing techniques of profit-seeking firms.