Finding optimal output and profit level

Not what you're looking for?

See the attached file.

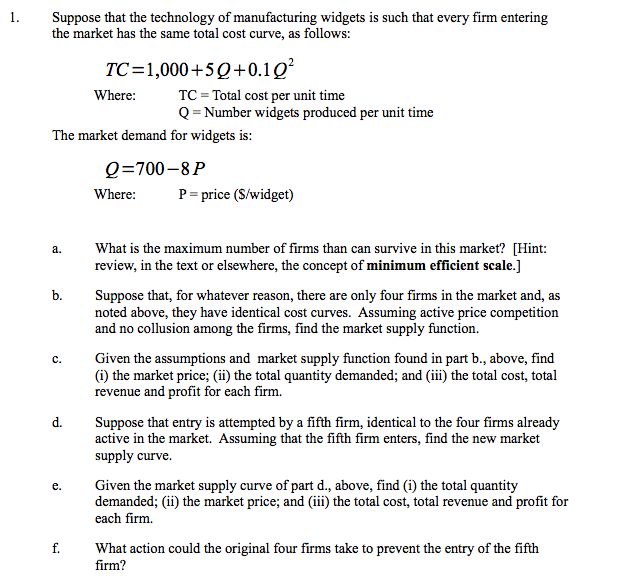

Suppose that the technology of manufacturing widgets is that every firm entering the market has the same total cost curve, as follows:

TC=1000+5Q+0.1Q^2

Where : TC=Total cost per unit time

Q=Number of widgets produced per unit time

The market demand for widgets is:

Q=700-8P

Where P=price ($/widget)

a. What is the maximum number of firms that can survive in the market?

b. Suppose that, for whatsoever reason, there are only four firms in the market and, as noted above, they have identical cost curves. Assuming active price competition and no collusion among the firms, find the market supply function.

c. Given the assumptions and market supply function found in part b., above, find (i) the market price; (ii) the total quantity demanded; and (iii) the total cost, total revenue and profit for each firm.

d. Suppose that entry is attempted by a fifth firm, identical to the four firms already active in the market. Assuming that the fifth firm enters, find the new market supply curve.

e. Given the market supply curve of part d., above, find (i) the market price; (ii) the total quantity demanded; and (iii) the total cost, total revenue and profit for each firm.

f. What action could the original four firms take to prevent the entry of the fifth firm?

{kind=link}

Purchase this Solution

Solution Summary

The solution describes the steps to calculate equilibrium market price and profits of firms existing in the market. It also studies the effect on the market and profits of firms if another firm attempts to enter the market.

Solution Preview

a) TC=1000+5Q+0.1Q^2

Marginal Cost=MC=dTC/dQ=5+0.2Q

Average Total Cost=TC/Q=(1000/Q)+5+0.1Q

d(ATC)/dQ =-(1000/Q^2)+0.1

Let us find the output level at which ATC has minimum value.

d(ATC)/dQ=0

-(1000/Q^2)+0.1=0

Q^2=10000

Q=100

Marginal Cost at Q=100 is given by

MC=5+0.2Q=5+0.2*100=$25

In price competitive environment, each firm sets its output level such that MC=P

Price, P=MC=$25

Demand at P=$25 is given ...

Education

- BEng (Hons) , Birla Institute of Technology and Science, India

- MSc (Hons) , Birla Institute of Technology and Science, India

Recent Feedback

- "Thank you"

- "Really great step by step solution"

- "I had tried another service before Brain Mass and they pale in comparison. This was perfect."

- "Thanks Again! This is totally a great service!"

- "Thank you so much for your help!"

Purchase this Solution

Free BrainMass Quizzes

Economics, Basic Concepts, Demand-Supply-Equilibrium

The quiz tests the basic concepts of demand, supply, and equilibrium in a free market.

Pricing Strategies

Discussion about various pricing techniques of profit-seeking firms.

Basics of Economics

Quiz will help you to review some basics of microeconomics and macroeconomics which are often not understood.

Economic Issues and Concepts

This quiz provides a review of the basic microeconomic concepts. Students can test their understanding of major economic issues.

Elementary Microeconomics

This quiz reviews the basic concept of supply and demand analysis.