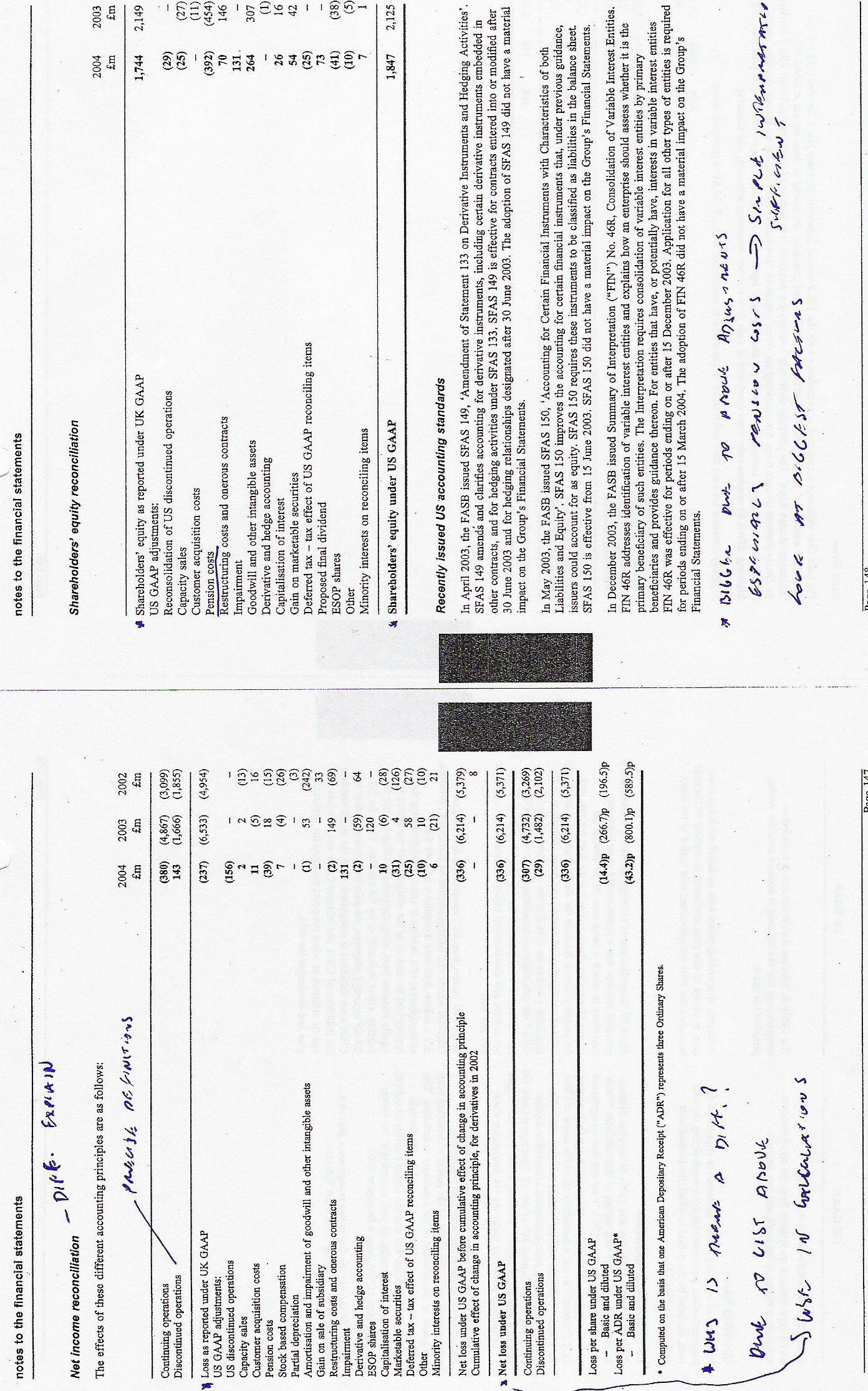

US, UK GAAP Accounting differences: discontinued operations, goodwill, intangibles, loss, interest capitalization

Not what you're looking for?

Write a commentary on the following items: US discontinued operations, goodwill and other intangible assets, restructuring costs and onerous contracts, capitalisation of interest. In your commentary you should demonstrate in each case your understanding of the reasons for the difference between:

Loss as reported under UK GAAP and net loss under US GAAP, and shareholders equity as reported under UK GAAP and shareholders equity under US GAAP.

(see attachment)

{kind=link}

Purchase this Solution

Solution Summary

The solution presents two scholarly articles which discuss the differences between US and UK GAAP accounting in a narrative format. The discussions include the items requested in the problem but also any other significant differences between the two country's accounting.

Solution Preview

In an effort to give you as much information as possible for your questions I have included two articles below.

Following are the differences between the UK and US GAAP that materially affected the companies' financial statements:

Goodwill and Intangible Assets: US GAAP required, Accounting Principles Board (APB) Opinion No. 17, that the excess of acquisition price over net assets acquired (goodwill) be amortized over its useful life, not exceeding forty years. US GAAP required similar treatment for other intangible assets such as brand names, licenses, trademarks and patents, etc. However, Financial Accounting Standards Board (FASB) Statement No. 142 superseded APB Opinion. According to the Statement, goodwill and intangible assets will not be amortized but tested for impairment and appropriate adjustments will be made.

UK companies were allowed to write off goodwill and intangible assets to reserves in the related financial period. However, since 1998, goodwill should be capitalized and amortized over its estimated useful economic life.

Income Taxes and Deferred Income Taxes: British companies are allowed to use the new tax rates as soon as they are proposed in the government budget. American companies are not permitted such treatment of tax rates until the enactment of proposed rates into law.

UK companies account for deferred income taxes only to the extent of management's judgment of probable liabilities or benefits that may materialize in the foreseeable future. US accounting standards require a detailed accounting for deferred income taxes.

Revaluation of Assets/Properties: UK accounting standards allow a revaluation of properties based upon their current market value. The US GAAP require that the properties be recorded in the financial statements on a historical cost basis, and allow any permanent decrease in the value to be expenses.

Several British companies in the sample revalued their properties. Any surplus resulting from revaluation was shown in the carrying value of assets and was taken directly to shareholders' equity or a revaluation reserve which was a part of shareholders' equity. Any deficit, in addition to the reflection in the carrying value of assets, was charged to the income statement.

Most of the companies' properties were carried on a higher value in comparison the historical cost basis required by the US GAAP. The properties' value, in most cases, had to be adjusted downward to bring them in compliance with the US GAAP.

A diversity in carrying value of properties also resulted in a different amount of depreciation charged to the income statement. Therefore, depreciation charges were modified usually reduced, in order to reconcile the differences.

Some companies in the sample did not charge depreciation on properties such as freehold and leasehold properties because, they believed, it was insignificant. In the US, all fixed assets, with the exception of land, should be amortized over their estimated useful lives.

The gain or loss on sale of properties was also affected because of the different methods used to value properties. UK companies recorded a gain or loss based on revalued carrying amounts and took it to the income statement. Any revaluation surplus was then realized and reclassified to retained earnings. The gain or loss on sale of properties was adjusted to reflect difference between sale proceeds and net carrying value based upon historical cost in order to bring it in conformity with US GAAP.

Dividends: UK companies provide for dividends, including proposed dividends awaiting shareholders' approval, in the related year. On the other hand, US companies provide for dividends in the year in which they are declared.

Convertible Capital Bonds: UK companies charged the costs incurred for issuance of convertible capital bonds to additional paid in capital. US GAAP require that such costs be deferred and amortized over the life of the bonds.

Employee Share Ownership Plan and Compensation Expenses: UK accounting standards allow recording of advances/loans granted to employees under employee share ownership plans as contingent liabilities. US GAAP require that such transactions be shown as a deduction from shareholders' equity.

I

n addition, US accounting standards require that compensation expenses should be recorded in case of issuance of share options or warrants to employees at cost. UK GAAP does not require such treatment. UK companies recorded compensation expenses in order to reconcile their financial statements to US GAAP.

Pension Costs: Several UK companies adjusted their pension costs in order to bring them in compliance with US GAAP. UK GAAP allows the measurement of pension plan assets at discounted present value of expected future income. US GAAP require that such assets be valued at their fair market values.

The US GAAP requires that plan assets and obligations be measured as of the date of the financial statements or within three months before the financial statements date. UK GAAP allows the valuation based upon the latest actuarial assessment.

Extraordinary Items: Some costs, such as restructuring and disposal of operations, that qualified as "exceptional items" and "extraordinary items" under UK accounting standards did not meet the criteria for extraordinary items, as outlined by the US GAAP. According to the US GAAP, a transaction must be unusual in nature and infrequent in occurrence in ...

Purchase this Solution

Free BrainMass Quizzes

Understanding the Accounting Equation

These 10 questions help a new student of accounting to understand the basic premise of accounting and how it is applied to the business world.

Writing Business Plans

This quiz will test your understanding of how to write good business plans, the usual components of a good plan, purposes, terms, and writing style tips.

Introduction to Finance

This quiz test introductory finance topics.

Basic Social Media Concepts

The quiz will test your knowledge on basic social media concepts.

Change and Resistance within Organizations

This quiz intended to help students understand change and resistance in organizations