Hedging using forward market and money market hedges

Not what you're looking for?

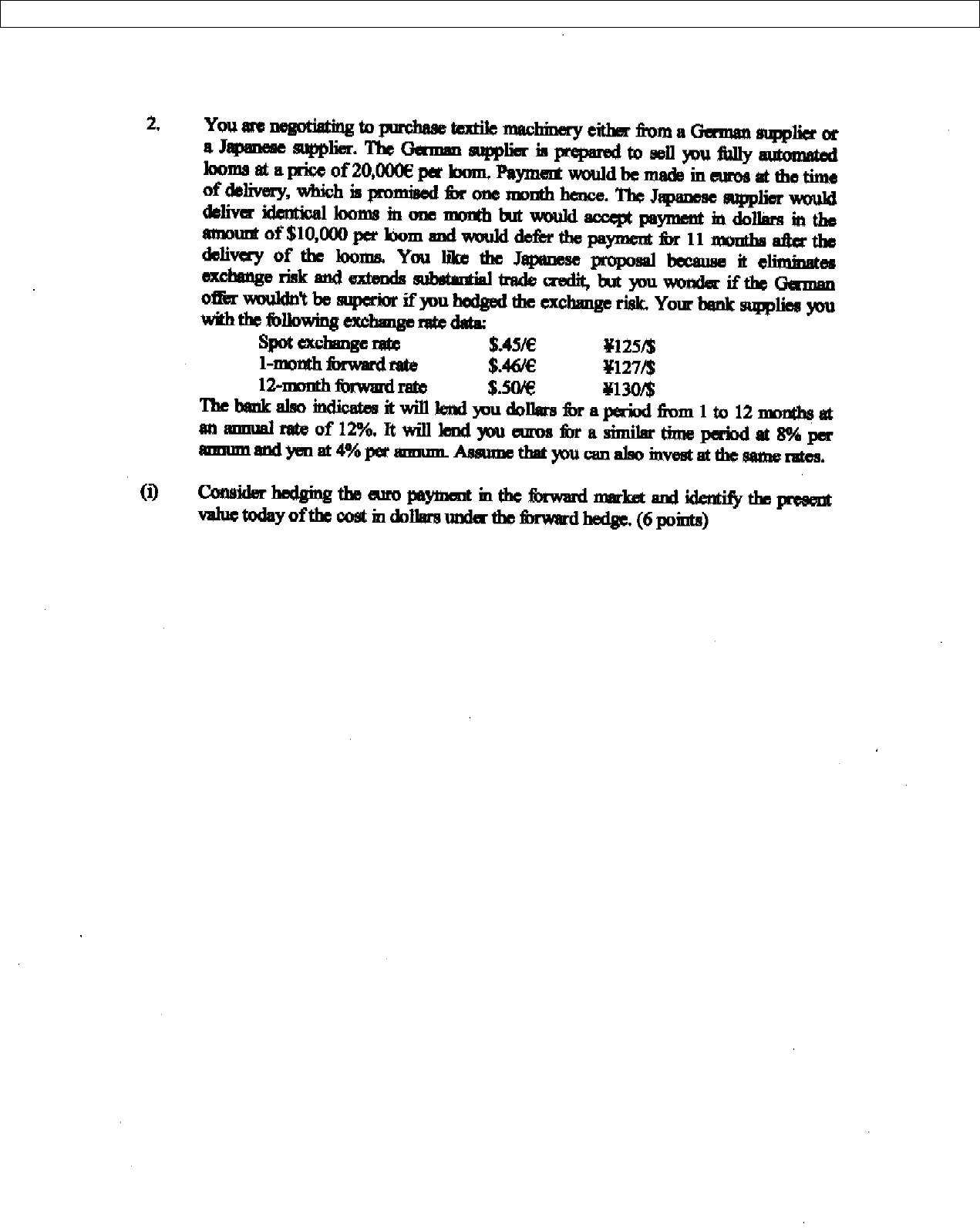

You are negotiating the purchase of textile machinery either from a German supplier or a Japanese supplier. The German supplier is prepared to sell you fully automated looms at a price of 20,000 Euros per loom. Payment will be made in Euros at the time of delivery, which is promised for one month hence. The Japanese supplier would deliver identical looms in one month but would accept payment in dollars in the amount of $ 10,000 per loom and would defer the payment for 11 months after the delivery of the looms. You like the Japanese proposal because it eliminates exchange risk and extends substantial trade credit, but you wonder if German offer wouldn't be superior if you hedged the exchange risk. Your bank supplies you with the following exchange rate data:

Spot exchange rate $.45/Euro Y 125/ $

1 month forward $.46/Euro Y 127/ $

12 month forward $.50/Euro Y 130/ $

The bank also indicates it will lend you dollars for a period from 1 to 12 months at an annual rate of 12%. It will lend you euros for a similar time period at 8% per annum and yen at 4% per annum. Assume that you can also invest at the same rates.

i) Consider hedging the euro payment in the forward market and identify the present value today of the cost in dollars under the forward hedge.

ii) Consider hedging the euro payment in the money market. Clearly identify the various steps and amount of dollars needed today for the spot hedge.

iii) To hedge the euro payment what must be your US dollar opportunity cost for you to be indifferent between a forward market hedge and a money market hedge?

iv) Find the cost of the Japanese loom and make your recommendations regarding a Japanese or German supplier.

{kind=link}

{kind=link}

{kind=link}

Purchase this Solution

Solution Summary

The solution answers questions on hedging using forward market and money market hedges.

Solution Preview

See attached file

Price Payment due

German supplier 20,000 Euro 1 month from now

Japanese supplier $10,000 12 month from now

Spot exchange rate $.45/Euro Y 125/ $

1 month forward $.46/Euro Y 127/ $

12 month forward $.50/Euro Y 130/ $

Bank interest rate

Dollar 12% per annum

Euro 8% per annum

Yen 4% per annum

i) Hedging the euro payment in the forward market

Buy 1 month forward euro

1 month forward $.46/Euro

20,000 Euro will cost $9,200

Present value of $9,200 will be obtained by discounting this payment by the dollar interest ...

Purchase this Solution

Free BrainMass Quizzes

Marketing Management Philosophies Quiz

A test on how well a student understands the basic assumptions of marketers on buyers that will form a basis of their marketing strategies.

Accounting: Statement of Cash flows

This quiz tests your knowledge of the components of the statements of cash flows and the methods used to determine cash flows.

Transformational Leadership

This quiz covers the topic of transformational leadership. Specifically, this quiz covers the theories proposed by James MacGregor Burns and Bernard Bass. Students familiar with transformational leadership should easily be able to answer the questions detailed below.

Understanding Management

This quiz will help you understand the dimensions of employee diversity as well as how to manage a culturally diverse workforce.

Basics of corporate finance

These questions will test you on your knowledge of finance.