Portfolio Return and Beta

Not what you're looking for?

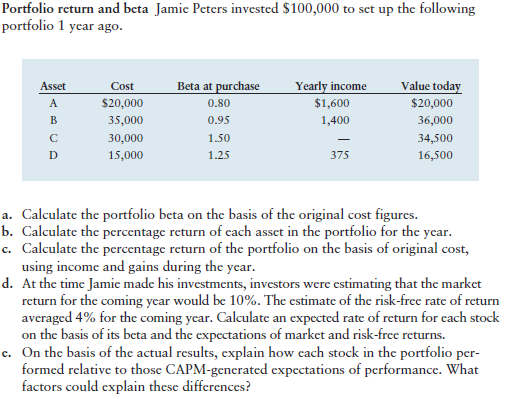

Jamie Peters invested $100,000 to set up the following portfolio 1 year ago. (see attachment for table).

a. Calculate the portfolio beta on the basis of the original cost figures.

b. Calculate the percentage return of each asset in the portfolio for the year/

c. Calculate the percentage return of the portfolio on the basis of original cost, using income and gains during the year.

d. At the time Jamie made his investments, investors were estimating that the market return for the coming year would be 10%. The estimate of the risk-free rate of return averaged 4% for the coming year. Calculate an expected rate of return for each stock on the basis of its beta and the expectations of market and risk-free returns.

e. On the basis of the actual results, explain how each stock in the portfolio performed relative to those CAPM-generated expectations of performance. What factors could explain these differences?

{kind=link}

Purchase this Solution

Education

- MPhil, Madurai Kamaraj University

- MCom, Annamalai University

- IATA, International Air Transport Association

Recent Feedback

- "Great explanations on how the answers were obtained."

- "Love the way she explains everything step by step."

- "Solutions were thoroughly explained."

- "Excellent explanations of how problems are solved"

- "Thanks"

Purchase this Solution

Free BrainMass Quizzes

Cost Concepts: Analyzing Costs in Managerial Accounting

This quiz gives students the opportunity to assess their knowledge of cost concepts used in managerial accounting such as opportunity costs, marginal costs, relevant costs and the benefits and relationships that derive from them.

Balance Sheet

The Fundamental Classified Balance Sheet. What to know to make it easy.

Production and cost theory

Understanding production and cost phenomena will permit firms to make wise decisions concerning output volume.

Business Ethics Awareness Strategy

This quiz is designed to assess your current ability for determining the characteristics of ethical behavior. It is essential that leaders, managers, and employees are able to distinguish between positive and negative ethical behavior. The quicker you assess a person's ethical tendency, the awareness empowers you to develop a strategy on how to interact with them.

Marketing Management Philosophies Quiz

A test on how well a student understands the basic assumptions of marketers on buyers that will form a basis of their marketing strategies.