Dividend Policy

Not what you're looking for?

Hi,

You have answered my problem 'cost of the capital' and I would like to ask you to help me with one more case if this possible.

Here is the new case for dividend policy.

Questions to be answered.

Please explain the calculations from the spreadsheet or any - I am having a trouble with few questions from the case. Briefly, but still, please explain your logic.

I am having a trouble with this topic.

Thank you.

**

After reading the text, please open the attachment for the tables and questions.

When you select 'printing option' you will get the regular size of the material from the attachment.

===

Subject: Dividend Policy

Case: Bessemer Steel Products, Inc

For over 70 years, Bessemer Steel Products, Inc has been a leading producer of various parts for automobiles, light trucks, and other vehicles. Its output is sold to the major automobile producers, auto supply companies, and repair shops. However, during the 1981 and 1982 recession, Bessemer's management concluded that the company should diversify in order to reduce risk and to enter markets with greater growth potential. Therefore, the decision was made to diversify into several totally new, but related, product lines.

Using substantial cash flows from profits and depreciation, and substantial unused debt capacity, Bessemer Steel's management resolved to seek only synergic acquisitions, which meant either companies in high-growth industries whose operations could be improved by Bessemer's expertise or those whose expertise would help Bessemer in its core operations. This suggested that acquisitions be sought primarily in the newly developing fields or robotics and material science. Thus, Bessemer acquired 3 robotics firms and 2 firms involved in metallurgical research and development.

These acquisitions produced the desired results - they strengthened Bessemer's research and development capabilities, helped it maintain and even expand its traditional business, and, most important. Enabled the company to expand into several profitable new areas. To illustrate, in the early 1980s, virtually all of the company's assets were invested in traditional automobile and light-truck body production. However, as a result of diversification program, by the end of 1992 these old product lines amounted to only 50% of assets, sales, and income, with the other 50% coming from new products and businesses, including a substantial amount of work in the space industry. The company is still interested in new acquisitions, and it is now investigating several potential candidates.

Other than during its first few years of operations, Bessemer has followed the practice of paying out approximately 60% of its earnings as cash dividends. Accordingly, dividends have fluctuated with earnings from year to year. In each annual report, the policy of paying out 60% of earnings has been retained, and this has given Bessemer a reputation for paying generous dividends. Because of its liberal dividend policy, Bessemer's stock is mainly owned by retired individuals, college endowment funds, income-oriented mutual funds, and other investors who are seeking high current income. The nature of its stockholders has been confirmed by several recent surveys conducted by the company - questionnaires completed by shareholders indicate clearly that they are income-oriented, and that, if anything, they would like to see the company increase its payout ratio.

The discussion continued for almost an hour past the scheduled adjournment time. It terminated only because Rite had to catch a plane to Berlin, where he was to make a presentation to a German industry group about newly developed materials for building extremely strong, rigid, but lightweight automobile bodies. Before adjourning, though, the board directed by Mary Dowd, vice president of finance, to have her staff study the dividend policy issue and to prepare a report for the next directors' meeting. Dowd was given explicit directions to consider the following alternative policies:

1. Continue the present policy of paying 60% of earnings.

2. Lower the present payout to some % below 60% - for example 20, 30, or 40% - and then keep the payout ratio constant at this new figure.

3. Set a relatively low regular dividend, such as 50 cents per share and then supplement it periodically with an extra dividend whose size would depend on the availability of funds and the company's need for capital. The size of the regular dividend would have to be determined at the outset, but all subsequent dividend decisions could be deferred, on a quarter-by-quarter basis, and made on the basis of knowledge of the company's cash flow position and prospects at the time of the dividend decision.

4. Establish a fixed dollar amount of dividends - for example- $1 dollar per share per year, payable 25 cents per quarter - and then, as earnings grow, increase the dividend. Under this plan, the payout ratio would fluctuate somewhat as earnings rose or fell in response to business cycle fluctuations, but the dividend would never be cut except in a dire emergency. If this policy were adopted, the question of the size of the initial dividend would also have to be settled. In addition, it would be useful to decide, at least tentatively, whether or not the company should plan to increase the dividend annually, and if so, at what rate? Eventually, management would have to determine how hard to strive to meet the growth target, because earnings will surely fall below the projected level in some future year.

The directors also asked Dowd to consider whether the dividend policy should be announced. Rite and Harris both expressed the opinion that the dividend policy should not be announced, citing the company's present's present position as an example of how an announced policy could cause the firm to feel 'locked in' and thus force it to take actions that otherwise would be undesirable. Mashburn and Brady, on the other hand, argued that stockholders, as owners of the company, ought to be told what management planned to do.

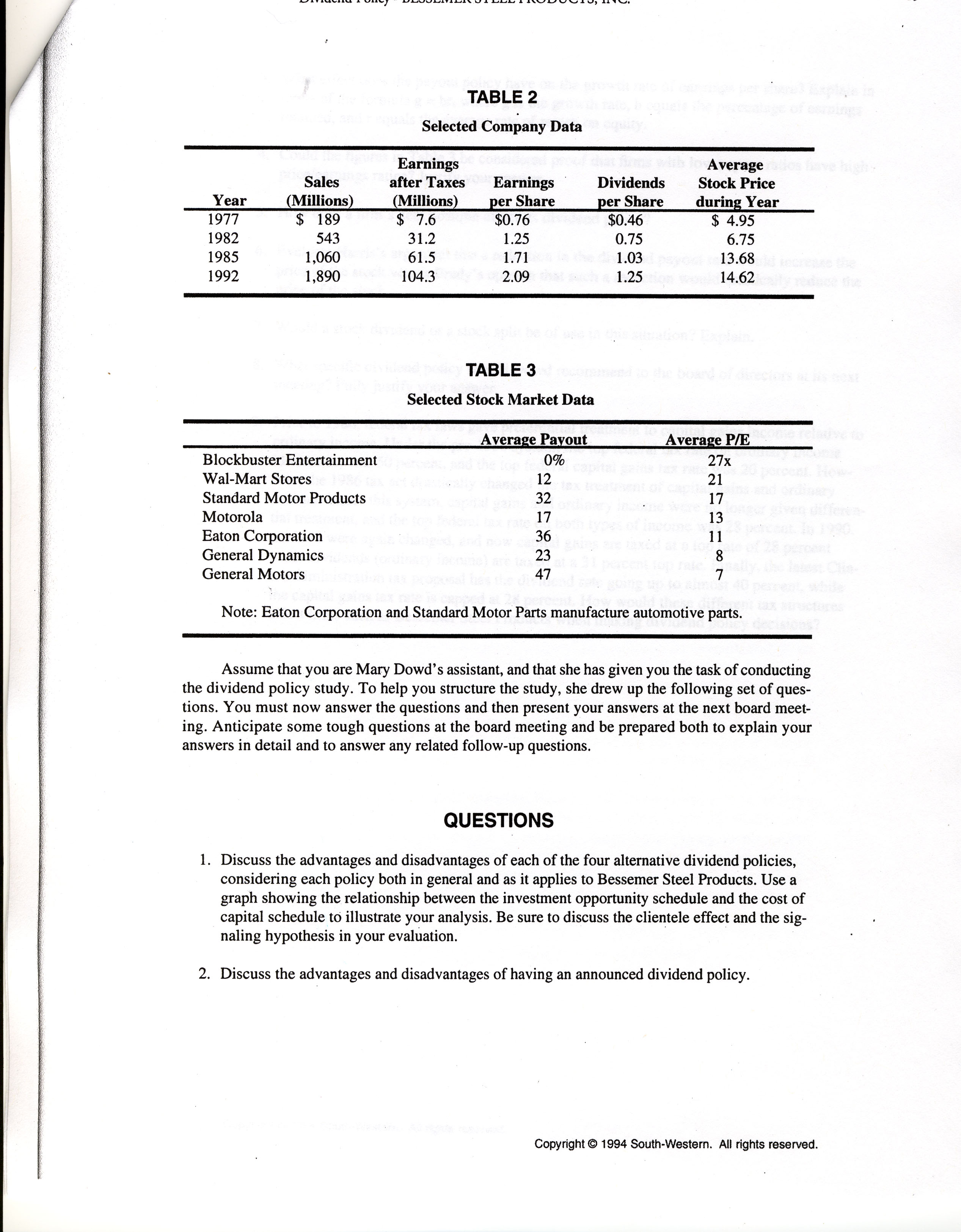

As Dowd was leaving the meeting, Harris asked her to include in her report an analysis of the firm's past growth rate in sales, total earnings, and earnings per share, as well as a statement of how earnings per share figures might have differed if the firm had followed a different payout policy [see Table 2]. Finally, Harris also promised to send Dowd some figures on payout ratios and price/earnings ratios that he had seen in a brokerage house report a few days before. He subsequently sent the figures shown in Table 3.

See Table 2 and Table 3 (see - attachment)

Assume that you are Mary Dowd's assistant, and that she has given you a task of conducing the dividend policy study. To help you structure the study, she drew up the following set of questions. You must now answer the questions and then present your answers as the next board meeting. Anticipate some tough questions at the board meeting and be prepared both to explain your answers in detail and to answer any related follow-up questions.

QUESTIONS (see the attachment)

--

{kind=link}

{kind=link}

Purchase this Solution

Purchase this Solution

Free BrainMass Quizzes

Situational Leadership

This quiz will help you better understand Situational Leadership and its theories.

Basics of corporate finance

These questions will test you on your knowledge of finance.

Marketing Management Philosophies Quiz

A test on how well a student understands the basic assumptions of marketers on buyers that will form a basis of their marketing strategies.

Organizational Leadership Quiz

This quiz prepares a person to do well when it comes to studying organizational leadership in their studies.

Income Streams

In our ever changing world, developing secondary income streams is becoming more important. This quiz provides a brief overview of income sources.