Braemar Saddlery: Under and Over Applied Overhead

Not what you're looking for?

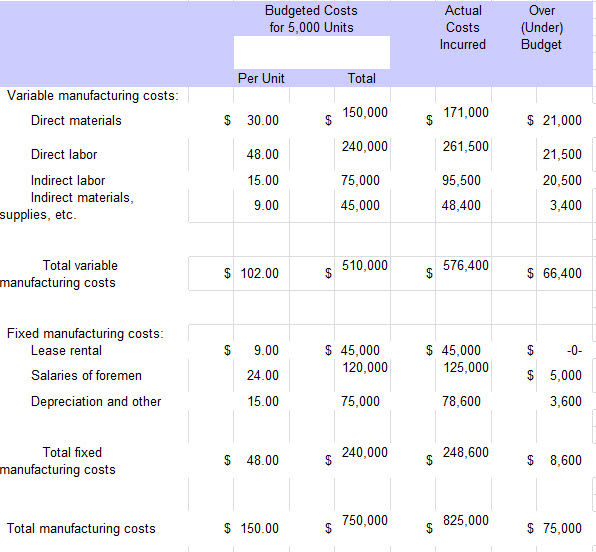

Braemar Saddlery uses department budgets and performance reports in planning and controlling its manufacturing operations. The following annual performance report for the custom saddle production department was presented to the president of the company:

Budgeted Costs for 5,000 Units Per Unit (see attached for better formatting)

Variable manufacturing costs:

Direct materials $ 30.00

Direct labor 48.00

Indirect labor 15.00

Indirect materials, supplies, etc. 9.00

Total variable manufacturing costs $ 102.00

Fixed manufacturing costs:

Lease rental $ 9.00

Salaries of foremen 24.00

Depreciation and other 15.00

Flexible Budget

Variable manufacturing costs:

Direct materials $ 150,000

Direct labor 240,000

Indirect labor 75,000

Indirect materials, supplies, etc. 45,000

Total variable manufacturing costs $ 510,000

Fixed manufacturing costs:

Lease rental $ 45,000

Salaries of foremen 120,000

Depreciation and other 75,000

Actual Costs Incurred

Variable manufacturing costs:

Direct materials $ 171,000

Direct labor 261,500

Indirect labor 95,500

Indirect materials, supplies, etc. 48,400

Total variable manufacturing costs $ 576,400

Fixed manufacturing costs:

Lease rental $ 45,000

Salaries of foremen 125,000

Depreciation and other 78,600

Over (Under) Budget

Variable manufacturing costs:

Direct materials $ 21,000

Direct labor 21,500

Indirect labor 20,500

Indirect materials, supplies, etc. 3,400

Total variable manufacturing costs $ 66,400

Fixed manufacturing costs:

Lease rental $ 0

Salaries of foremen $ 5,000

Depreciation and other 3,600

Although a production volume of 5,000 saddles was originally budgeted for the year, the actual volume of production achieved for the year was 6,000 saddles. Direct materials and direct labor are charged to production at actual cost. Factory overhead is applied to production at the predetermined rate of 150 percent of the actual direct labor cost.

After a quick glance at the performance report showing an unfavorable manufacturing cost variance of $75,000, the president said to the accountant: "Fix this thing so it makes sense. It looks as though our production people really blew the budget. Remember that we exceeded our budgeted production schedule by a significant margin. I want this performance report to show a better picture of our ability to control costs."

Instructions

a. Prepare a revised performance report for the year on a flexible budget basis. Use the same format as the production report above, but revise the budgeted cost figures to reflect the actual production level of 6,000 saddles. (Leave no cells blank - be certain to enter "0" wherever required. Under-budget amounts should be indicated with a minus sign. Round your per unit answers to 1 decimal place. Omit the "$" sign in your response.)

b. What is the amount of over- or underapplied manufacturing overhead for the year? (Note that a standard cost system is not used.)

Manufacturing overhead applied $

Underapplied manufacturing overhead $

{kind=link}

Purchase this Solution

Solution Summary

Your tutorial is attached in excel. Click in cells to see computations. This guidance shows you the process for over and under applied as well as flexible budget computations.

Education

- BSc, University of Virginia

- MSc, University of Virginia

- PhD, Georgia State University

Recent Feedback

- "hey just wanted to know if you used 0% for the risk free rate and if you didn't if you could adjust it please and thank you "

- "Thank, this is more clear to me now."

- "Awesome job! "

- "ty"

- "Great Analysis, thank you so much"

Purchase this Solution

Free BrainMass Quizzes

Marketing Management Philosophies Quiz

A test on how well a student understands the basic assumptions of marketers on buyers that will form a basis of their marketing strategies.

Production and cost theory

Understanding production and cost phenomena will permit firms to make wise decisions concerning output volume.

Introduction to Finance

This quiz test introductory finance topics.

Organizational Behavior (OB)

The organizational behavior (OB) quiz will help you better understand organizational behavior through the lens of managers including workforce diversity.

Paradigms and Frameworks of Management Research

This quiz evaluates your understanding of the paradigm-based and epistimological frameworks of research. It is intended for advanced students.