Flexible Budget of Activity Based Costing

Not what you're looking for?

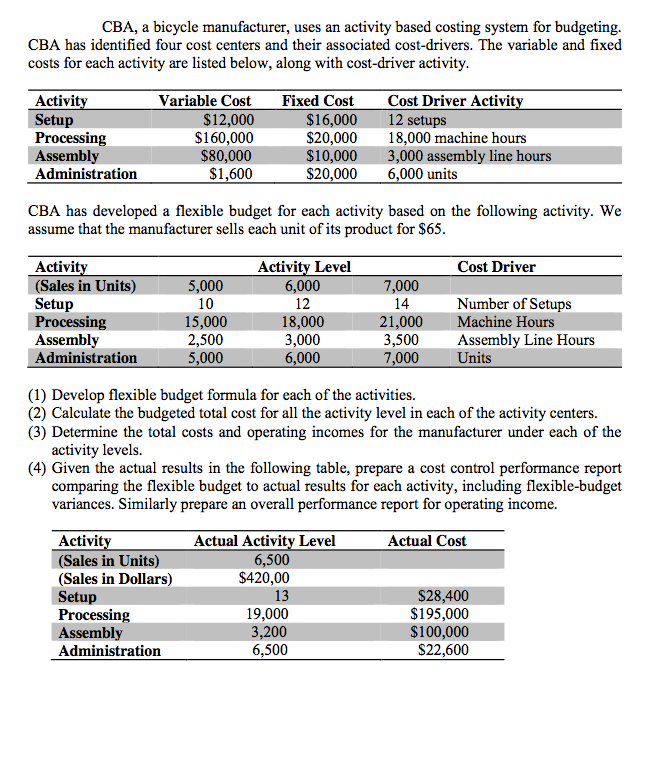

CBA, a bicycle manufacturer, uses an activity based costing system for budgeting. CBA has identified four cost centers and their associated cost-drivers. The variable and fixed costs for each activity are listed below, along with cost-driver activity.

Activity

Processing Administration

Variable Cost

$160,000 $1,600

Fixed Cost

$20,000 $20,000

Cost Driver Activity

18,000 machine hours 6,000 units

Setup  $12,000

$16,000 12 setups

Assembly $80,000

$10,000 3,000 assembly line hours

CBA has developed a flexible budget for each activity based on the following activity. We assume that the manufacturer sells each unit of its product for $65.

Activity

Setup Assembly

Activity Level

10 12 14 2,500 3,000 3,500

Cost Driver

Number of Setups Assembly Line Hours

(Sales in Units) 5,000

6,000 7,000

Processing 15,000

18,000 21,000 Machine Hours

Administration 5,000

6,000 7,000 Units

(1) Develop flexible budget formula for each of the activities.

(2) Calculate the budgeted total cost for all the activity level in each of the activity centers.

(3) Determine the total costs and operating incomes for the manufacturer under each of the

activity levels.

(4) Given the actual results in the following table, prepare a cost control performance report

comparing the flexible budget to actual results for each activity, including flexible-budget variances. Similarly prepare an overall performance report for operating income.

Activity

(Sales in Dollars) Processing Administration

Actual Activity Level

$420,00 19,000 6,500

Actual Cost

$195,000 $22,600

(Sales in Units)

6,500

Setup

13 $28,400

Assembly

3,200 $100,000

{kind=link}

Purchase this Solution

Solution Summary

A solution to an activity based costing accounting question. Comparing actual results with flexible budget.

Solution Preview

(1)

Flexible budget formula for each activity

Setup = 16,000 + 1,000 (i.e. 12,000/12) * per setup

Processing = 20,000 + 8.89 (i.e. 160,000 /18,000) * per machine hour

Assembly = 10,000 + 26.67 (i.e. 80,000/3,000) * per assembly line hour

Administration = 20,000 + 0.27 (i.e. 1,600/6,000) * per unit

(2)

Activity Level = 5,000

Setup = 16,000 + 1,000 * 10 = 26,000

Processing = 20,000 + 8.89 * 15,000 = 153,350

Assembly = 10,000 + 26.67 * 2,500 = 76,675

Administration = 20,000 + 0.27 * 5,000 = 21,350

Total Cost = 26,000 + 153,350 + 76,675 + 21,350 = 277,375

Activity Level = 6,000

Setup = ...

Purchase this Solution

Free BrainMass Quizzes

Organizational Behavior (OB)

The organizational behavior (OB) quiz will help you better understand organizational behavior through the lens of managers including workforce diversity.

Cost Concepts: Analyzing Costs in Managerial Accounting

This quiz gives students the opportunity to assess their knowledge of cost concepts used in managerial accounting such as opportunity costs, marginal costs, relevant costs and the benefits and relationships that derive from them.

Change and Resistance within Organizations

This quiz intended to help students understand change and resistance in organizations

Understanding the Accounting Equation

These 10 questions help a new student of accounting to understand the basic premise of accounting and how it is applied to the business world.

Social Media: Pinterest

This quiz introduces basic concepts of Pinterest social media