Regress Dividend Payments

Not what you're looking for?

The first file is the 2 problems; the second file is the data for the first problem; and the third is the data for the second problem.

Problems must be completed in SAS, or STATA.

See the attached file.

{kind=link}

Purchase this Solution

Solution Summary

Regress dividend payments are highlighted and the problem is solved with the details provided.

Solution Preview

I've attached two word documents with the SAS code and comments included. In the first excercise you are looking at the effects of male vs. female models, but more importantly you are looking at the effects from using AHE82 vs. AHE (which has been adjusted for inflation I suspect). The model with AHE fits much better. Also, look at the signs and magnitudes of the coefficients and consider their effect on the dependent variable.

In exercise two, you are looking at a plain vanilla OLS model and comparing it to a model with seasonal effects via dummy variables. This is a nice exercise to help understand the properties of time series data (i.e. seasonality and time trend issues).

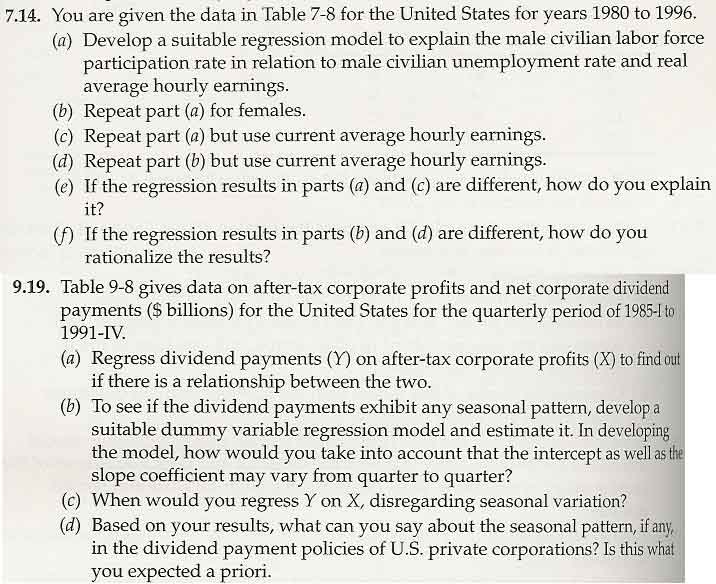

Exercise 7.14

SAS setup

DATA labor_1;

set labor;

run;

part A)

Here I am just looking at some descriptive stats for the data.

proc means data=labor_1 n mean median std var min max;

var clfprm clfprf unrm unrf ahe82 ahe;

run;

The MEANS Procedure

Variable N Mean Median Std Dev Variance Minimum Maximum

ƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒ

CLFPRM 17 76.0941176 76.300 0.6859943 0.4705882 74.900 77.400

CLFPRF 17 55.8882353 56.600 2.5670709 6.5898529 51.500 59.300

UNRM 17 6.9117647 6.900 1.3896413 1.9311029 5.200 9.900

UNRF 17 6.8058824 6.600 1.2477332 1.5568382 5.400 9.400

AHE82 17 7.6105882 7.680 0.1655850 0.0274184 7.390 7.810

AHE 17 9.3700000 9.280 1.5229412 2.3193500 6.660 11.820

ƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒƒ

Here's a quick look at the histogram of the dependent variable to check that it's normally distributed.

proc univariate data=labor_1;

histogram clfprm /anno=labor_1 normal(color=blue)

cfill=grey midpoints=73 to 79 by .1;

run;

Here are is another graphical test for normality of the dependent variable.

proc univariate data=labor_1 noprint;

var clfprm;

qqplot / normal(mu=est sigma=est color=red);

run;

Again we check for a quadratic relationship between the dependent variable and the independent ...

Purchase this Solution

Free BrainMass Quizzes

Economics, Basic Concepts, Demand-Supply-Equilibrium

The quiz tests the basic concepts of demand, supply, and equilibrium in a free market.

Pricing Strategies

Discussion about various pricing techniques of profit-seeking firms.

Elementary Microeconomics

This quiz reviews the basic concept of supply and demand analysis.

Basics of Economics

Quiz will help you to review some basics of microeconomics and macroeconomics which are often not understood.

Economic Issues and Concepts

This quiz provides a review of the basic microeconomic concepts. Students can test their understanding of major economic issues.