How Materiality impacts the Type of Audit Report

Not what you're looking for?

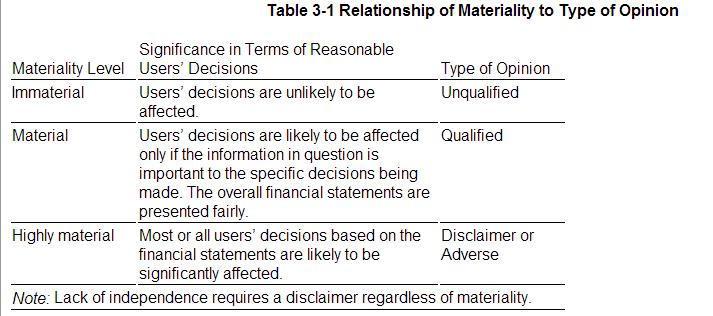

Review Table 3-1 in Ch. 3 of Auditing and Assurance Services. How does the relationship of materiality and opinion affect the way you work with a client?

The Table 3-1 Relationship of Materiality to Type of Opinion is attached.

{kind=link}

Purchase this Solution

Solution Summary

Your discussion is 264 words and discusses how materiality impacts client interactions during an audit and how the audit adjustments impact the type of report.

Solution Preview

The relationship between materiality and opinion does not really impact the audit work but does impact the client on a practical level. Regardless of this natural link between materiality and audit report, materiality must be established during the planning phase and then used as a benchmark during testing. Then, items that are not GAAP but below materiality threshold are reviewed with the client but they have the OPTION of whether they book ...

Education

- BSc, University of Virginia

- MSc, University of Virginia

- PhD, Georgia State University

Recent Feedback

- "hey just wanted to know if you used 0% for the risk free rate and if you didn't if you could adjust it please and thank you "

- "Thank, this is more clear to me now."

- "Awesome job! "

- "ty"

- "Great Analysis, thank you so much"

Purchase this Solution

Free BrainMass Quizzes

Change and Resistance within Organizations

This quiz intended to help students understand change and resistance in organizations

Learning Lean

This quiz will help you understand the basic concepts of Lean.

Income Streams

In our ever changing world, developing secondary income streams is becoming more important. This quiz provides a brief overview of income sources.

MS Word 2010-Tricky Features

These questions are based on features of the previous word versions that were easy to figure out, but now seem more hidden to me.

Basics of corporate finance

These questions will test you on your knowledge of finance.